[The following article is the fifth instalment in a series.]

5. The Adani Group and International Capital

The year 2023 was a tumultuous one for the Adani Group of companies. In January 2023, according to a report by the US research firm Hindenburg, the Adani Group was worth $218 billion, and Adani had a personal net worth of $120 billion, making him the world’s third richest person.

The Hindenburg Research report appeared a year ago, on January 24, 2023. It labeled the Adani group “the largest con in corporate history”.[1] Share prices of firms in the group plummeted: the market valuation of the group as a whole fell by $150 billion. So did Adani’s personal wealth (comprised mainly of the shares of his own companies). Financial markets considered there was a serious risk of default on Adani borrowings: The market price of 2024 Adani Green Energy dollar bonds (September 2024 maturity) on international exchanges dropped from $95.19 on January 24 to $63.05 on February 2.

However, over the past year the group’s share prices, and Adani’s own wealth, have recovered to a large extent. As of January 2024, the combined market value of the group has risen to just $47 billion below the pre-Hindenburg price.[2] Adani has climbed back up the Bloomberg Billionaire Index, to no. 12, a few steps below his position a year ago. On any given day, depending on the daily fluctuations of share prices, either he or Mukesh Ambani is the richest person in India. The 2024 Adani Green Energy dollar bond is now trading at $97.61.[3]

We do not aim to go here into the various aspects of the Adani phenomenon, which would require a book-length study. We look here at a limited question: what, if anything, did Adani’s crisis and his recovery signify about his relationship with international capital and the West? In what way are India and Indian businessmen making their presence felt in the world?

“A wholesale assault on India and Indians”

As mentioned earlier (in the first instalment of this article), the Adani group made out that the Hindenburg report was an attack on India.

This is not merely an unwarranted attack on any specific company but a calculated attack on India, the independence, integrity and quality of Indian institutions, and the growth story and ambition of India.[4]

The Chief Financial Officer of the Adani group, Jugeshinder Singh, an Australian citizen, released a video of him standing next to the Indian flag.[5] In an interview, he likened the Hindenburg report to the Jallianwala Bagh massacre of Indians by the British Raj:

In Jallianwala Bagh, only one Englishman gave an order, and Indians fired on other Indians. So am I surprised by the behaviour of some fellow Indians? No. A white person gave an order that some Indians should fire is a possibility.[6]

The former Solicitor General of India, Harish Salve, who has represented both the Indian government and the Adani group, and now resides and practises in London, termed the Hindenburg report “a wholesale assault on India and Indians.” He traced its cause to the fact that “Nobody is happy at the fact that India… is making its presence felt in the world. Nobody is happy that Indian businessmen are making their presence felt in the world….”[7]

In the view of the Rashtriya Swayamsevak Sangh organ, the Organiser, the Hindenburg report was

part of the fifth generation warfare wherein hostile powers use various oblique tactics to target the Indian economy…. India is now growing economically and expanding its wings to get control over critical infrastructure assets overseas. It is also working on undermining the dominance of the US Dollar by promoting UPI and Rupee trade. Besides, India has not succumbed to the coerced pressure of the West (read: the US and the EU ) and has been continuing trade with Russia by importing Ural Crude and settling trades in Indian Rupee and other non-Dollar currencies. In such an eventuality, India must be well prepared to confront many more similar attacks.[8] [matter in round brackets in the original]

This implies, then, that Adani represents Indian national capital, which is under attack from international capital, which is jealous of Indian national capital’s growth.

On the other hand, for many of Adani’s critics, his meteoric rise epitomised ‘crony capitalism’. This was a phrase used by Western economists in the wake of the Southeast Asian crisis of 1997-98 to denote a deviation from ‘true’ competitive capitalism. This deviation, they claimed, had been hidden from Western eyes by opaque Asian business practices, including businessmen’s family links and political patronage. Media in the West today make out a similar case about the Adani phenomenon.

Contrary to both the above views, our view is as follows:

(1) While Adani’s rise has been particularly meteoric, it is broadly in line with the pattern of the development of Indian big business since the days of British rule.

(2) Adani’s business empire has grown under the overall policy-frame promoted by international capital in India for the last three decades, including privatisation of infrastructure, State largesse to private capitalists in the form of land and resources, and debt-fueled expansion of the corporate sector.

(3) In fact, nothing in the Adani business model brought it into contradiction with international capital. India’s finance-driven infrastructure boom of the 2000s, of which Adani was a part, actually expanded the market for international firms, and provided profitable opportunities for international finance.

(4) Moreover, in recent years, the Adani group has increasingly relied on foreign borrowings for its growth. While its investments will yield revenues only in the medium-term, its borrowings are short-term, and need to be rolled over periodically. These two facts – its dependence on foreign borrowings, and the mismatch between its assets and its short-term liabilities – made it vulnerable to doubts in the minds of foreign lenders. This is the vulnerability Hindenburg targeted.

(5) International investors have been aware for some time about the Adani Group’s high levels of debt, and about allegations of financial manipulations, including round-tripping of capital. In assessing the group’s ability to pay, international investors have banked precisely on its claimed proximity to those in power (‘cronyism’), and not on its corporate governance or the state of its finances.

(5) Adani’s efforts since the Hindenburg report have been focussed on restoring his credibility with foreign investors. In this he has had considerable success, even as some financial challenges await him in 2024.

(6) Adani has been closely tied to US’s strategic drive, in India, Sri Lanka, and West Asia. In the last few months, these ties have been further strengthened, conveying an endorsement of the Adanis by the US itself.

Below we elaborate these points.

Adani structure not unusual for Indian big business

In the case of Southeast Asia, the ‘crony capitalism’[9] theory diverted attention from the more obvious explanation of the crisis: Those economies had recently opened themselves to volatile inflows and outflows of international financial capital.[10] Similarly, while cronyism surely exists, it should not divert us from the important role of international capital in the phenomenal growth of Adani.

The Hindenburg report found the labyrinthine financial structure of the Adani Group, and the flows of capital across its group firms and across borders, suspicious. But these are not unusual for Indian big business houses. There are historical roots to this: In India, monopoly capital did not develop out of competitive capitalism. Rather, it emerged under colonial rule, as native entrepreneurs, who were entrenched in the trading castes and communities, sought out business opportunities within the colonial economy. They mastered the arts of arranging finance for business ventures, controlling markets for inputs and products, and obtaining State support and protection for themselves. These patterns survived the formal end of British rule. A 1970s study concluded that “monopoly capital in India bears a closer family resemblance to pre-industrial monopolies than to contemporary monopoly capitalism in the west”.[11]

Since the days of British rule, Indian big business has been structured principally as family-controlled groups. Rather than develop monopolies in specific industries/sectors, they have spread their activities across diverse, indeed unrelated, sectors, from soap to steel to power-generation to real estate. The binding cord has been their ability to arrange funding for these diverse ventures; and the focus of their activities has been finance, not production.

To maintain personal control over their diverse businesses in the period of globalisation, Indian big business houses have used complex financial structures, with cross-holdings among a large number of associated firms. For example, a study found the following number of entities (including business arms, subsidiaries, joint ventures, associated companies and other ‘promoter group’ companies) of four major business groups in March 2018: Adani – 182; A.V. Birla – 168; Reliance – 227; and Tata – 738. (Of these, the following numbers were foreign entities: Adani – 41; A.V. Birla – 81; Reliance – 57; and Tata – 540.)[12] Financial globalisation has greatly facilitated Indian business houses’ longstanding practice of transferring funds abroad illicitly from their Indian firms. A portion of these funds returns in the guise of investment by foreign portfolio investors, a practice known as ‘round-tripping’.

Indian big business and international capital

Those who claim that international capital is unhappy with the rise of Adani subscribe to the false notion that, merely by increasing in size, Indian big businesses pose a challenge to international capital.

Unlike the big bourgeoisie of Japan, which developed in the late 19th century under Japanese rule, the big bourgeoisie of India, which arose under British rule, did not overcome its dependence on imports of machinery. To this day it remains considerably dependent on repeated technology imports. In this fashion the growth of the Indian big bourgeoisie also boosts the market for multinational corporations, and as such is not a challenger to them. For example, during the boom of the 2000s, as private firms entered power generation on a large scale, power equipment imports rose steeply. Similarly, as the telecom industry in India has undergone spectacular growth, it has remained heavily dependent on imports, not only for telecom equipment but even handsets (or components thereof, for merely assembling here).[13] The trade deficit on account of power generating equipment rose more than 4 times between 2001 and 2008; in the case of telecom equipment, it rose more than 9 times.[14]

Take India’s airline industry, catering to the upper segment of Indian society: Along the chaotic course of its development, marked by the launching of many airlines, spectacular bankruptcies and eventual domination by just two firms, the industry has constituted a rich market for the world’s two major airplane manufacturers, Boeing and Airbus. In February 2023 the Indian Prime Minister announced that the newly-privatised Air India, now owned by the Tata Group, would buy 470 new aircraft – 250 from the Airbus (Europe) and 220 from Boeing (US).

Media coverage of the Air India mega-deal almost universally cited the huge order as evidence of India’s economic rise. Airbus CEO Guillaume Faury said the size of the order “demonstrates the appetite for growth in the Indian aviation industry. It’s the fastest growing in the world.” But the order is a bonanza for US and European manufacturing, not Indian manufacturing. US President Biden declared: “The United States can and will lead the world in manufacturing… This purchase will support over one million American jobs across 44 states, and many will not require a four-year college degree.” British Prime Minister Rishi Sunak said that “This landmark deal…. will create better-paying jobs and new opportunities in manufacturing hubs from Derby to Wales, so we can grow the economy…”

In June 2023 Indigo trumped Air India by placing an even larger order, for 500 Airbus planes. So large are the combined orders by the two Indian firms that Airbus and Boeing may have difficulty finding sufficient workers to build them.[15]

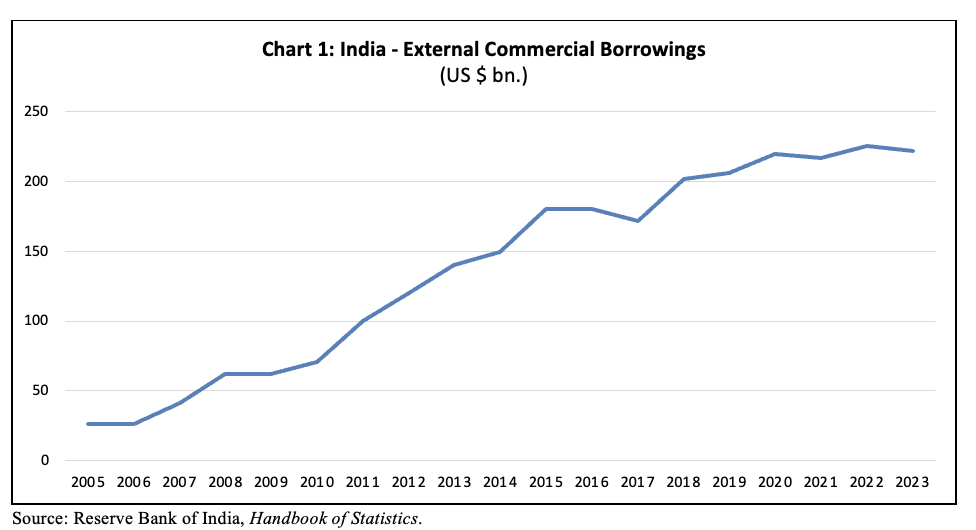

While it is admittedly difficult to build a domestic aircraft manufacturing industry, this phenomenon of import dependence is not restricted to aviation, nor to power and telecom, but characterises much of Indian large industry. During the boom of 2004-11, not only did India’s imports of machinery and equipment rise, but the share of imports in the domestic market for capital goods too rose.[16] That is, dependence actually grew with the boom. To finance their import requirements, Indian firms often obtain external commercial debt. Such debts have mounted more than eight times in dollar terms since 2005 (see Chart 1). These debts are to be serviced in foreign currencies.

Shifting infrastructure into the private sector

The 2000s witnessed the rapid growth of private investment in infrastructure in India, with the Adani group just one of several groups witnessing rapid growth in this way. This growth took place despite the riskiness of infrastructure and its low revenues (infrastructural investments have a long gestation period, in which the firms have no revenues with which to service the debt; the prices of infrastructure are regulated by the State;[17] and changes in Government policy have a large impact on the sector).

Till the 1980s infrastructure worldwide was generally in the public sector. It was with the rise of neoliberalism in the 1980s that countries began privatising infrastructure, and provided the private firms various types of subsidies and guarantees to attract them to infrastructure. In India, private investment in infrastructure really took off in the 2000s. The reason was the flood of global finance: After falling into recession in 2001, the US and other developed countries tried to stimulate their economies by expanding credit massively, which wound up flowing around the world. International investors borrowed cheap in, say, the US or Japan, and invested the borrowed funds in Indian stock markets, or lent them on to Indian borrowers. International investors made handsome margins on such ‘carry trade’. Thus it was the ‘push’ factor from international capital that led to private capital inflows into India rising to 10 per cent of GDP by 2007-08.[18]

Foreign inflows trigger credit boom, which expands private infrastructure

These inflows triggered a credit boom in India. (The incoming foreign currency was bought up by the Reserve Bank of India, releasing rupees in exchange; this resulted in a rise in bank deposits. This meant in turn that banks were impelled to increase their lending steeply.) The Economic Survey 2016-17 summarised it thus:

Firms launched new projects worth lakhs of crores, particularly in infrastructure-related areas such as power generation, steel, and telecoms, setting off the biggest investment boom in the country’s history. Within the span of four short years, the investment-GDP ratio had soared by 11 percentage points, reaching over 38 percent by 2007-08. This investment was financed by an astonishing credit boom, also the largest in the nation’s history, one that was sizeable even compared to other large credit booms internationally. In the span of just three years, running from 2004-05 to 2008-09, the amount of non-food bank credit doubled. And this was just the credit from banks: there were also large inflows of funding from overseas, with capital inflows in 2007-08 reaching 9 percent of GDP. All of this added up to an extraordinary increase in the debt of non-financial corporations.[19]

When the Global Financial Crisis of 2008 led to a dip in GDP growth in India, the Indian government pressurised the banks to further lend to infrastructure firms, thereby reviving growth within a year. This revival continued till about 2011-12. To reiterate, none of this growth posed any challenge to international capital, either industrial or financial. Various costs of this breakneck growth, in the form of forcible land acquisitions, destruction of the environment and privatisation of public assets, were borne by the Indian people.

The credit boom inevitably turned into a gargantuan problem of bad debt and stalled projects (these debts were largely written off by public sector banks in subsequent years). The Economic Survey 2014-15 acknowledged that “the evidence points towards over-exuberance and a credit bubble as primary reasons… for stalled projects in the private sector.”[20] Total “stressed assets” (bad debts) rose by 2017 to nearly 20 per cent of loans at public sector banks.[21]

In 2012 Credit Suisse brought out a report, House of Debt.[22] It found that the growth of bank loans was “increasingly being driven by a select few corporate groups”, with over 20 per cent of incremental loans contracted by just 10 groups – Adani, Essar, GMR, GVK, JSW, Jaypee, Lanco, Reliance ADA (Anil Ambani), Vedanta and Videocon. Most of their investments were in infrastructure, particularly power, and metals. Their debt had jumped five times in the past five years, to 13 per cent of total bank loans and 98 per cent of the net worth of the banking system.

The celebrated rapid GDP growth of 2003-11 was inseparable from the even more rapid growth of private corporate debt (and the private capture of natural resources and public assets; but that is a separate story). None of the above 10 groups grew by pioneering new technology. Nor did they exploit any ‘comparative advantage’ of India’s, such as cheap labour, either manual labour (as in readymade garments) or technical labour (as in the IT industry). These groups, including Adani, could flourish when a flood of finance overflowed from the developed countries. Once the economic downturn set in after 2008, the loans of the boom period began turning into bad debt.

Credit Suisse suggested asset sales as a possible panacea to resolve the debt crisis. In the following period, the crises in most of these groups intensified, with several unable to service their debts and some flagship firms going into insolvency. Many did indeed sell their assets to other firms. (Public sector banks, which had been directed to advance these loans, recovered very little from these sales, which were at a fraction of the value of the loans.)

However, the Adani group continued to acquire assets[23] and “in fact added to its towering debt pile”, which doubled between 2012 and 2019.[24] Many of these assets were acquired by Adani from other groups facing default, such as the Anil Ambani Reliance Group, the GMR Group, the Thapar Group and the GVK Group. Thus the debt crisis actually worked to further concentrate assets in Adani’s hands, as he continued to enjoy access to finance under a new government at the Centre in 2014. A commentator in 2019 wrote: “[A]s recently as 2013, most of the group’s assets were located in Gujarat. Six years later, it straddles most parts of India.”[25]

As the corporate sector defaulted on loans, these loans turned into the ‘non-performing assets’ (NPAs) of the banks. Banks then cut back on lending to industry, particularly infrastructure. (In Chart 2 above, lending to infrastructure firms, as a percentage of total bank lending, rises steeply till 2011, then levels off, and finally declines after 2015.)

Adani Group turns to direct foreign borrowing

In the post-2015 period, when domestic banks were unable or unwilling to lend more for infrastructure, the Adani group turned to direct[26] foreign borrowing in a big way, mainly in the form of foreign bonds, as well as loans from foreign banks for specific projects. For foreign investors, the Adani group’s heavy indebtedness, falling operating margins and return on capital invested were not a deterrent, given the group’s proximity to power. An Economic Times headline in the run-up to the general elections of 2014 read: “Gautam Adani, the baron to watch out for if Narendra Modi becomes king.”[27]

Bloomberg reported in 2019 that the Adani Group’s target was to raise the proportion of its foreign currency debt to 65 per cent over the next few years.[28] Indeed, in the following years the group’s debt profile changed rapidly. For the top five companies of the group, the share of bonds rose to 37 per cent of the total (of this, foreign bonds accounted for 29 per cent), and borrowing from international banks rose to 18 per cent. Thus, by March 2022, foreign borrowings directly contracted by the group accounted for 47 per cent of total borrowing (29+18=47).[29]

Adani Group’s Changing Debt Profile

Between 2015 and 2021, six different Adani Group companies raised about $10 billion through 18 US-dollar-denominated bond sales marketed and underwritten by US and European investment banks – yielding what Forbes called “juicy fees” for these banks.[30] The debt of the top five companies of the group rose by Rs 83,600 crore between March 2019 and March 2022 (excluding loans from related parties and other companies within the group).[31] Of this growth in debt, 56 per cent was on account of foreign bonds alone.

Apart from foreign bonds, the group also raised loans from foreign banks. According to the Adani Group response to the Hindenburg report, “The portfolio has developed deep domestic and international bank relationships…. This has strengthened access to diverse funding sources and structures.” Barclays, Deutsche Bank and Standard Chartered Bank, which Adani refers to as his “relationship banks”, fully funded the group’s takeover of a cement business from the Swiss firm Holcim in 2022. The Adani Group provides the following image of the debt for the Holcim takeover:

The running thread of the group’s response to Hindenburg is precisely to reassure international investors that it enjoys a close relationship with international capital – the group has “marquee investors like TotalEnergies, IHC, QIA, Warburg Pincus etc.”; “TotalEnergies, one of the leading integrated energy players globally, has strategic alliance with the Adani portfolio across its four verticals”; “The portfolio has developed deep domestic and international bank relationships”; it has “deep access to international bond markets and infrastructure investors”, and so on.[32]

How much did foreign lenders know?

Were foreign lenders unaware of the Adani Group’s financial situation? Investors in foreign bonds are not babes in the woods but large institutions equipped with an army of research analysts. When bond offerings are marketed to them by global investment banks, they do their own homework before subscribing. The following charts show the low operating margins and high share of cash flow from debt for the flagship firm, Adani Enterprises, in three periods (note: in 2015 the firm underwent a restructuring).[33]

Source: Aswath Damodaran, https://aswathdamodaran.blogspot.com/2023/02/control-and-complexity-deconstructing.html, February 4, 2023. “LTM” = last 12 months, i.e. January–December 2022.

Research analysts would have noted that the Adani Group lacked a ‘cash cow’, similar to the Tata Group’s software firm TCS or the Reliance Group’s petroleum business, to fund its giant ambitions.[34] A detailed two-part article in 2019 by M. Rajshekhar,[35] pointing to dense cross-holdings and inter-corporate loans between firms within the group, should have caused analysts to probe further. Yet the Adani Group faced no difficulty in raising an additional Rs 46,700 crore of foreign bonds in the following three years.

Most of the material on which the Hindenburg Research report was based has long been in the public domain. Not even its main argument was new as such: that is, the alleged use of offshore front companies to jack up the price of Adani shares, and thereby facilitate foreign borrowing. The essential facts were known in financial circles well before January 2023 (see Appendix 1). That did not prevent the Adanis from continuing to raise money.

The crucial consideration

Despite questioning the heavy debt load and the opaque financial transactions of the group, the Fitch Ratings research outfit, Credit Sights, acknowledged that the Adani Group had “solid banking relationships with both domestic and international banks, which have been willing to lend to the group large amounts for both its existing businesses and new ventures;” and further the Group “has been able to tap the US dollar bond markets repeatedly and raised debt at reasonable rates”, much of it in the previous two years.

Why were banks and international investors willing to lend, despite all the warning signs? The Credit Sights report is frank: “there are policy tailwinds supporting the development of such infrastructure assets… increased government support for these infrastructure projects could translate into better growth opportunities and financing conditions…. Gautam Adani also enjoys healthy relations with the ruling Modi administration. Mr Adani and Indian Prime Minister Narendra Modi know each other well, going back to the latter’s days as Chief Minister of Gujarat state.” (emphasis added) Evidently it was the very factors which are labeled ‘crony capitalism’ that made the Adani Group bankable. Given that guarantee, it was, and continues to be, profitable for international finance to do business with the Adani Group.

One striking evidence of the above argument is the contrast between foreign investment in Adani equity and in Adani foreign bonds:

— The major foreign portfolio investors, who own a substantial stake in most major Indian firms listed on the stock exchanges, have steered clear of Adani company shares. Almost all the foreign investment in Adani shares comes from a few murky foreign investors based in Mauritius, who are alleged to be fronts for the Adanis themselves. Evidently the ‘regular’ foreign investors in India’s share markets felt that the sky-high prices of Adani Group shares were not justified. (Aswath Damodaran, a leading valuation expert, analysed the finances of Adani Enterprises in February 2023 and arrived at a valuation of Rs 945 per share even on an optimistic basis; whereas the end-2022 price of the share was four times higher, at Rs 3,858.[36])

— At the same time, however, Adani Group companies were able to borrow heavily through foreign currency bonds, pledging their shares as security. Foreign investors subscribed to these bonds, even as they must have suspected that the true value of the pledged shares was much lower. Thus foreign investors extended loans (through bonds) not on the basis of the pledged shares, but on the basis of the clout the Adani Group commanded in the new India. As long as that clout continues, their investments remain secure.

Adani sets about reassuring international investors

The Hindenburg Research report raised the alarm regarding a whole range of issues concerning the Adani Group.[37] It had its intended shock effect. As investors feared default, the market price of bonds of the Adani group dropped steeply by February 1, so much so that investors could expect a return of 30 per cent if they picked up the bonds on global markets (compared to an average yield on such bonds of 5 per cent). Three international banks said they would no longer accept Adani bonds as collateral. Adani was immediately called upon to top up the collateral he had provided a group of banks for a $1 billion loan.

However, importantly, no Adani bonds were to mature in 2023; $1.9 billion would fall due in 2024, which gave the Adani Group some breathing time. In the months following the Hindenburg report, the group took a series of steps to reassure international investors (see Box)

Confidence of international capital largely restored

The Adani Group propagated all of these developments as evidence of the confidence of international investors in the group. Indeed it seems they are reassured. As we mentioned at the outset, the Adani Group firms’ bonds are now trading at pre-Hindenburg prices. Secondly, after the Hindenburg report, the French firm Total, the largest foreign direct investor in the Adani Group,[38] had put on hold its plan to invest an additional $5 billion in Adani Enterprises’ green hydrogen projects. By the end of 2023, it appears Total has returned to investing in the group’s ‘clean energy’ ventures.

The Adani Group continues to face some challenges. A February 2023 analysis of the group’s financial situation found that it was over-extended on short-term borrowings in the year ending March 2023 itself, and it faced a large liquidity gap.[39] It remains to be seen how the group has addressed this issue, and how it will complete its committed expenditure toward debt repayments and capital expenditure in the coming period. To the extent that the share prices of its firms have fallen since January 2023, the Adani Group would have been called on to pledge additional shares against loans they have received from foreign lenders. The group’s share prices have recovered considerably, but on a cumulative basis, the group’s market capitalisation is reported to be 24 per cent below its pre-Hindenburg figure.[40]

Nevertheless, it is clear that the confidence of foreign creditors and investors is largely restored.

Strategic bond with the US

The Adani Group has forged a special bond with the US, making itself a part of US global strategy. In turn the US has given it a special place in its plans for the entire belt between India and Europe.

Solar energy: Adani’s focus on ‘green energy’ ties in with the current drive of the US to out-compete China in solar and other renewables technology. The US and India have entered into a “US-India Strategic Clean Energy Partnership”. In both the US and India, market competition has been set aside, tariff and non-tariff barriers are set up against lower-priced Chinese equipment, and subsidies are provided subsidies for domestic production of solar equipment, as well as for electricity produced from such equipment. In such areas, the Indian government’s aim of promoting domestic production through its ‘Atmanirbhar’ programme does not go against Western interests, since the overwhelmingly dominant producer of solar equipment, through the entire supply chain, is China (its share in all manufacturing stages of solar panels, such as polysilicon, ingots, wafers, cells and modules exceeds 80 per cent, which is double China’s share of global demand in these commodities).[41] Any increase in domestic production would displace Chinese imports.

Adani claimed in June 2020 that, with his solar projects, “the 90 per cent import of Chinese equipment will fall to 50 per cent, and ultimately zero. In 3-5 years, it will be negligible.”[42] As yet that has not proved the case: in fact, as India has tried to ramp up its solar power production, imports of solar panels, most of all from China have surged in 2023. Bloomberg reports that some Indian manufacturers are concerned about the possibility of China restricting the export of machinery to make wafers, cells and modules.[43] Nevertheless, Adani Enterprises has completed two stages of the supply chain – a pilot plant to make polysilicon ingots, and production of India’s first wafers.

Indeed, as India seeks to reduce its dependence on China for energy-related equipment and commodities, opportunities may open up for western firms. India’s Production-Linked Incentives scheme to promote domestic manufacturing in solar equipment and in energy storage would lead Indian firms to seek tie-ups with foreign technology providers.[44] At the same time, Indian renewable energy firms, including Adani, are planning to invest in the US to capture some of the $369 billion in subsidies offered in the US’s 2022 Inflation Reduction Act.[45]

US strategy for Indian Ocean and beyond: The US has been promoting the Adani group as part of its strategy for the Indian Ocean and West Asian region.

— In July 2022 an Adani-led joint venture with the Israeli Gadot group acquired the lease for Haifa Port. Haifa is Israel’s leading port, handling half the country’s freight volume in 2021.[46] Haifa is also a refuelling stop for the US Navy Sixth Fleet, and it hosts a naval base housing Israel’s nuclear submarine fleet. When a Chinese state-owned firm won the nearby Haifa Bay Port in 2015, the US objected. In May 2020, then Secretary of State Mike Pompeo applied pressure on Israel to call off infrastructure projects with China.[47]

Adani made a very high bid of $1.2 billion for the Haifa lease, 55 per cent more than the next bid, and 36 per cent higher than what the Israeli government had expected.[48] It is clear that Adani viewed the acquisition as a strategic one for his firm. He may also have been informed of the strategic plans of the US and India for the region, which were made public rather later, in September 2023.

Adani tweeted: “Delighted to win the tender for privatization of the Port of Haifa in Israel with our partner Gadot. Immense strategic and historical significance for both nations! Proud to be in Haifa, where Indians led, in 1918, one of the greatest cavalry charges in military history!” (He was referring to fact that, in 1918, the 15th Imperial Service Cavalry Brigade, comprised of troops from India’s princely states, participated in the British attack on Haifa Port. Indian soldiers, including the commander of the Indian contingent, died in this battle in the service of the British empire, which captured the port from the Ottoman empire.)

— As discussed in the previous section of this article, in September 2023, the US announced the India-Middle East-Europe Economic Corridor (IMEEC). The starting point of the corridor is the Adani port of Mundhra in Gujarat; the mid-point is the Adani port in Haifa. As we noted there, the IMEEC is intended to fuse US strategic interests, Israel’s ‘normalisation’ plans, India’s rivalry with China, and the growth plans of the Adani business house.

The last leg of the IMEEC extends from Haifa to Greece. The US has been applying pressure on Greece, which had earlier sold the Athens port of Piraeus to the Chinese firm COSCO Shipping, to distance itself from China. This pressure was stepped up under Trump, and has continued under Biden. On a September 2020 visit to Greece, Pompeo said he raised the question of “the Chinese Communist Party’s attempts to use economic power here and in the region to gain strategic leverage over European democracies.” The US ambassador to Greece said China itself had identified Greece as “the dragon’s head of the Belt and Road Initiative in Europe”.[49]

In August 2023, the Greek press reported that Adani was looking to take over a Greek port and turn it into a gateway to Europe. The ports of Kavala, Volos and Alexandroupoli were mentioned. In August, Modi visited Greece, the first Indian prime minister to do so in four decades. According to the Greek press, during talks with Greek prime minister Kyriakos Mitsotakis, Modi expressed interest in India’s acquiring ports in Greece.[50]

— Finally, the US International Development Finance Corporation announced on November 8, 2023 that it would led Adani Ports $553 million to establish a deepwater shipping-container terminal at the Port of Colombo in Sri Lanka. Adani will develop the port with Sri Lankan partners. Crisis-hit Sri Lankan has been the arena for a tussle between the west and India, on the one hand, and China on the other. Chinese banks and engineering firms had built a deepwater port at the Rajapaksa stronghold of Hambantota; when Sri Lanka failed to service the loan, ownership of the port and nearby land were transferred to China under a 99-year lease. However, Colombo Port is perhaps 25 times larger. The New York Times comments that “The Biden administration’s willingness to go into business with the Adani Group might burnish the company’s reputation abroad. Karan Adani said the port deal was a ‘reaffirmation by the international community of our vision, capability and our governance.’”[51]

The above are examples of India “getting control over critical infrastructure assets overseas”, but with the help of a superpower.

Explanations for the Hindenburg episode

Why, finally, did Hindenburg Research attack Adani? One simple explanation is that Hindenburg, as a ‘short-seller’ (a firm that makes a speculative bet that the price of a share will fall), would stand to gain by a fall in Adani Group share prices. In that case, it would have been an isolated incident with few other ramifications.

However, given that Hindenburg Research had never taken on a target of this size, given the large investment it made in researching the group, and given the timing of the report (at the same time as the BBC documentary on the Gujarat riots of 2002 appeared, and the US was applying pressure regarding India’s stand on the Ukraine war), it is probable that there was a strategic link. As we recounted in the first part of this article, George Soros’s speech at the Munich Security Conference directly targeted Adani and linked him to Modi (“their fate”, he said, “is intertwined”), and questioned Modi’s ties to both “open and closed societies” (i.e., the West and Russia). The attack on Adani served as one more reminder to the Indian government of how the US and its allies could target the Indian government and those close to it. However, having demonstrated its capabilities, the US stepped back; the Indian government too stepped back; and ties between the two revived with even greater strength.

In conclusion

To sum up: the relationship between the Adani Group and international capital underwent strains during 2023. These strains were projected by the Adani Group and its supporters as an attack on Indian national capital by western imperialism. The same strains were viewed by some critics of the Adani Group as the exposure and debacle of crony capitalism. However, as we have seen,

— the Adani Group has posed no threat to international capital; instead, it opens up profitable opportunities for it in multiple ways. The group’s initial growth was part of the Indian economy’s boom/bubble of the 2000s, which was fueled by large inflows of foreign capital.

— In more recent years, the Adani Group has funded its runaway growth through foreign debt, much of it short-term debt. Foreign lenders were willing to lend to the group, not on the basis of its financials, but precisely on the basis of its closeness to power (‘cronyism’).

— After the initial shock of the Hindenburg Research report, the group has focussed on measures to revive the confidence of international capital in its creditworthiness, and in this it has largely succeeded.

— Finally, explicit backing by the US to the Adani Group, as part of overall US strategy for the region and beyond, will further boost ‘international confidence’ in the group.

It is a separate question that India’s present path of development, which has proved so beneficial to both international capital and the Adani Group, works to the detriment of the Indian people, who constitute the Indian nation; but that is a separate story, which we cannot adequately address here.

[To be continued]

______________________________________________________________________________________

Appendix 1: Well before Hindenburg

Most of what appears in the Hindenburg report is based on material in the public domain. Further, reports by media outlets and market research had raised red flags well before Hindenburg.

One of the main contentions of the Hindenburg report concerned the use of front companies to raise the price of Adani Group shares, and thereby facilitate foreign borrowing. The steps were as follows:

(1) In order to raise foreign borrowings, the promoters of the Adani Group pledged a portion of their shares.

(2) Opaque foreign portfolio investors (FPIs) invested in shares of Adani Group firms, thereby jacking up the prices of these shares. Hindenburg alleges that these FPIs were actually controlled by the Adanis themselves (through funds the Adanis had somehow transferred abroad in the past). These FPIs invested almost exclusively in Adani Group shares, and stayed invested, unlike most FPIs, which spread their investments among many firms, and regularly sell their holdings when prices rise, in order to book profits.

(3) These manipulated high share prices allowed the Adanis to pledge a smaller portion of their shareholding than otherwise would have been the case.

(4) Indian stock market regulations require that a firm which is listed on the market ensure that at least 25 per cent of its shares are held by the public, i.e. the promoters may not hold more than 75 per cent. Hindenburg alleged that, through their benami FPI holdings, the Adanis actually breached the 75 per cent limit. As a result the percentage of genuinely ‘free-float’ shares, i.e. available to the public, was less than 10 per cent in the Adani Group firms, even as low as 2 per cent. Thus there was no true ‘market price’, but only a manipulated price, for these firms’ shares.

— However, in April 2021 itself, the online journal The Morning Context published a detailed article[52] on seven FPIs which invested almost exclusively in shares of Adani firms, but, despite the share prices reaching all-time highs, never sold any shares to book profits. All seven were registered in the tax haven Mauritius. Three of them shared the same address in Mauritius. The article pointed out that “such fund structures… give rise to suspicion of round-tripping – i.e. that it is the promoters of the company who have routed their own money through overseas jurisdictions and tax havens into funds that invest in their own companies.” The higher valuation, it noted, “aids in raising fresh capital”.

— On June 14, 2021, the Economic Times reported that the National Securities Depository Ltd (NSDL) had frozen the accounts of three of the above mysterious foreign investors in Adani Group companies (the three that shared a single Mauritius address).[53] The news caused a panic in the market, and prices of Adani Group company shares immediately fell between 5 and 25 per cent. The shares recovered after the NSDL quickly clarified that it had not frozen the accounts. The London-based Economist noted the event, but downplayed its significance, claiming that foreign investors invested through Mauritius to “cope with India’s extensive, bewildering and intrusive tax regime”. Adani’s prospects, the Economist said, “appear bright”, and “The group counts giants like Total, a French oil supermajor, and Qatar’s sovereign-wealth fund as junior partners in various joint ventures.”[54]

— In August 2022, the Fitch Ratings research firm Credit Sights firm published a report: “Adani Group: Deeply Overleveraged”[55] (“leverage” refers to indebtness). It said “Over the past few years, the Adani Group has pursued an aggressive expansion plan that has pressurized its credit metrics and cash flows. The Adani Group is increasingly venturing into new and/or unrelated businesses, which are highly capital intensive and raises concerns regarding spreadin execution oversight too thin. We see little evidence of promoter equity capital injections into the group companies, which we feel is needed to reduce leverage in their stretched balance sheets.”

The report noted that “Some foreign investors in Adani Group stocks also include certain opaque funds, such as Albula Investment Fund, Cresta Fund and APMS Investment Fund, all of which are registered at the same address in Port Louis, Mauritius… A shareholding structure dominated by the Promoter Group and foreign portfolio investors, some of which are quite opaque… is quite unusual for such large-cap stocks.”

Credit Sights warned that “Excessive debt and overleveraging by the group could have a cascading negative effect on the credit quality of the bond issuing entities within the group…”

[1] Hindenburg Research, “Adani Group: How The World’s 3rd Richest Man Is Pulling The Largest Con In Corporate History”, January 24, 2023, https://hindenburgresearch.com/adani/

[2] Reuters, “India’s Adani Group signs deals to invest $1.49 bln in Telangana”, January 17, 2024.

[3] On January 17, 2024. https://www.boerse-frankfurt.de/bond/xs2383328932-adani-green-energy-ltd-4-375-21-24

[4] Adani Response, January 29, 2023.

[5] “Statement from Adani Group CFO Jugeshinder Singh on Hindenburg Research’s report”, https://www.youtube.com/watch?v=wH6jMHv_HqI.

[6] Swaraj Singh Dhanjal, Anirudh Laskar and Satish John, “Each one of Hindenburg’s allegations is a lie: Adani’s Jugeshinder Singh”, Mint, January 30, 2023.

[7] “Nobody is happy that India’s businessmen are making their presence felt in the world: Harish Salve”, https://www.youtube.com/watch?v=fwsXuplgSoA

[8] Sumeet Mehta and Binay Kumar Singh, “Hindenburg-Adani Controversy: Attack on Adani is continuation of assaults on Indian economy”, Organiser, February 5, 2023

[9] The term ‘crony capitalism’, to the extent it implies a non-crony capitalism as the norm in today’s world, is misleading. Contrary to the theories peddled in the wake of the Southeast Asian crisis, ‘cronyism’, in the form of the personal influence of individual capitalists or firms over the State, characterises most of contemporary world capitalism, to one extent or the other. Cronyism of a different type operates in the US itself, where a revolving door exists between Wall Street and the US Treasury (as also between weapons manufacturers and the State and Defense Departments). Political lobbying in the US is a legitimate industry that, in 2014, employed 100,000 persons and billed $9 billion a year. Lee Fang, “Where Have All the Lobbyists Gone?”, The Nation, March 10, 2014. The specific forms and methods of cronyism, however, do vary between the advanced capitalist countries and the Third World (the currently fashionable term for the latter is ‘emerging economies’). The complex networks of influence, family connections and opaque practices which Western economists claimed to be shocked to find in Southeast Asia are common to most Third World countries, waiting to be discovered post-facto by those economists whenever a crisis erupts in a particular country.

[10] See Jayati Ghosh and C.P. Chandrashekhar, Crisis as Conquest: Learning from East Asia, 2001.

[11] N.K Chandra, “Monopoly Capital, Private Corporate Sector and the Indian Economy, 1931-76”, August 1979, re-printed in The Retarded Economies: Foreign Domination and Class Relations in India and Other Emerging Nations, 1988.

[12] Surajit Mazumdar, “The Multi-Entity Structure and Control in Business Groups”, MPRA, December 2018.

[13] See Rahul Varman, Indian Telecom’s Spectacular Rise and the Nature of Monopoly Capital in India, Aspects of India’s Economy, no. 80, May 2023, https://rupeindia.wordpress.com/2023/05/05/aspects-of-indias-economy-no-80/, in particular Chapter IV and Appendix.

[14] Sudip Chaudhuri, “Manufacturing Trade Deficit and Industrial Policy in India”, Economic and Political Weekly (EPW), February 23, 2013.

[15] Siddharth Philip, Julie Johnsson and Anthony Palazzo, “IndiGo, Air India’s record plane order deliveries may not be an easy ride for Airbus, Boeing”, Bloomberg, June 22, 2023.

[16] Sudip Chaudhuri, “Import Liberalisation and Premature Deindustrialisation in India”, EPW, October 24, 2015.

[17] Since the costs of infrastructure feed into all other production costs and living costs, and since infrastructural firms are often natural monopolies (where there is no competitive price), the State generally regulates the prices of infrastructural services.

[18] R. Nagaraj, “India’s Dream Run, 2003-08: Understanding the Boom and Its Aftermath”, Economic and Political Weekly, May 18, 2013.

[19] Economic Survey 2016-17, vol. I, p. 86.

[20] Economic Survey 2014-15, vol. I, p. 70.

[21] Economic Survey 2016-17, vol. I, p. 88.

[22] Credit Suisse Asia Pacific/India, House of Debt, August 2, 2012.

[23] Credit Suisse Asia Pacific/India, House of Debt: Still in the Woods, October 21, 2015.

[24] Aman Kapadia and Forum Bhatt, “Adani’s Growing Debt Pile Is Changing Colour”, Bloomberg, November 5, 2019.

[25] M. Rajshekhar, “From 2014 to 2019: How the Adani Group’s footprint expanded across India,” Scroll, May 15, 2019.

[26] The Adani group had earlier indirectly taken foreign currency loans: the loan would be raised by an Indian bank, and lent on to, say, Adani Enterprises or Adani Power.

[27] April 10, 2014.

[28] Aman Kapadia and Forum Bhatt, op. cit.

[29] CLSA, Adani: Where Does the Debt Sit?, January 26, 2023.

[30] John Hyatt, “Behind The Adani Group’s ‘House Of Cards’: Juicy Fees For Wall Street Banks”, Forbes, January 26, 2023.

[31] Excluding related party transactions and inter-corporate loans within the group. Data from CLSA, op. cit.

[32] Adani Response.

[33] In 2015 Adani Enterprises unwound its holdings in Adani Ports and Power. Following this, the invested capital, revenues and operating incomes of the firm were smaller in 2016, rising thereafter. Data are taken from the spreadsheet provided in Aswath Damodaran, “Control, Complexity and Politics: Deconstructing the Adani Affair!”, https://aswathdamodaran.blogspot.com/2023/02/control-and-complexity-deconstructing.html

[34] M. Rajshekhar, op. cit.

[35] M. Rajshekhar, op. cit. and “From 2014 to 2019: How the Adani Group funded its expansion”, Scroll, May 16, 2019.

[36] Damodaran, op. cit.

[37] Such as the pledging of shares to raise debt; investigations regarding fraud and tax evasion; the moving of billions of dollars across a labyrinth of entities and shell firms; undisclosed related party transactions; breaching of limits on promoter holding, and stock price manipulation; and so on.

[38] In 2019, Total had bought a 37.4 per cent stake in Adani Gas (renamed Adani Total Gas) and a 50 per cent stake in Adani’s LNG project at Dhamra. In 2021 Total invested $2.5 billion to buy a 20 per cent of Adani Green as well as a 50 per cent stake in a solar farms joint venture with Adani Green.

[39] Hemindra Hazari, “The Adani Group has a significant liquidity gap to bridge”, February 27, 2023. https://www.smartkarma.com/insights/adani-group-has-a-significant-liquidity-gap-to-bridge

[40] Press Trust of India, “Year after Hindenburg: Adani claws back narrative on biz fundamentals”, January 24, 2024.

[41] International Energy Agency, Special Report on Solar PV Global Supply Chains, 2022.

[42] “We’ll edge out Chinese gear in 3-5 years: Gautam Adani,” Economic Times, June 10, 2020.

[43] Rajesh Kumar Singh, “Indian solar industry still heavily reliant on Chinese imports”, Bloomberg, December 15, 2023.

[44] According to the US International Trade Administration, “The U.S. market share of India’s energy-related equipment and commodities imports remains low. China was the top foreign competitor for low-cost equipment, but since 2020 India has sought to reduce its supply chain dependence on China, signaling increased opportunities for U.S. companies. The PLI scheme for solar and energy storage led several large Indian renewable energy companies and public sector entities to scout for partnerships with foreign technology providers. Large Indian energy companies like Adani, Renew Power, and Avaada, and public sector entities like Coal India Ltd. and NTPC Ltd., indicate interest in investing and diversifying into the clean energy space, including solar, energy storage, hydrogen, and smart grid technologies. The PLI scheme has prompted several U.S. solar companies to rethink their India strategy, and some have now established offices in India.

…[T]he annual market for stationary and mobile batteries in India is expected to grow to $6 billion by 2030, based on conservative estimates, and could surpass $15 billion…. Currently, U.S. energy storage technology enjoys a global competitive advantage, but suppliers will likely need to establish strong relationships with local business partners to enter this fast-developing market.” https://www.trade.gov/country-commercial-guides/india-renewable-energy

[45] Dipka Bhambhani, “Biden Looks to India to Help Counter China Clean Energy Dominance,” Forbes, December 11, 2023.

[46] Sabena Siddiqui, “What Adani’s Haifa port purchase means for India-Israel ties and the Arab region”, The New Arab, August 5, 2022.

[47] Shubhdha Choudhary, “Haifa Port Acquisition by Adani Group: Challenges Remain”, Bharat Shakti, January 7, 2024, https://bharatshakti.in/haifa-port-acquisition-by-adani-group-challenges-remain/

[48] Sabena Siddiqui, op. cit.

[49] Stuart Lau, “US pushes Greece to stop acting as China’s ‘dragon’s head’ into Europe”, November 3, 2020.

[50] Paul Antonopoulos, “Adani’s interest in Greek ports, Indian tourism, and labour policy – What did Mitsotakis and Modi discuss?”, Greek City Times, August 26, 2023.

[51] By Skandha Gunasekara and Alex Travelli, “U.S. Finance Agency Lends to Sri Lankan Port to Counter Chinese Influence”, New York Times, November 8, 2023.

[52] Jayshree P. Upadhyay, “Why do these foreign funds love Adani Group companies?”, The Morning Context, April 26, 2021.

[53] Pavan Burgula and Nehal Chaliawala, “Accounts of 3 FPIs owning Adani Group shares frozen”, Economic Times, June 14, 2021.

[54] “A strange news report briefly rattles the Adani Group”, Economist, June 19, 2021.

[55] August 23, 2022. https://www.slideshare.net/HindenburgResearch/creditsights-adani-group-23-august-2022p df